Comparing Closing Costs

Beware! Some lenders may quote low interest rates with a high cost! Learn how to weigh points or loan fees, closing costs, and prepaid items.

While savvy consumers search for the best mortgage interest rate, home loan estimates can be difficult to decipher. Many lenders quote interest rates and closing costs with little explanation.

To clarify, banks and mortgage companies don't have just one interest rate we can offer every day. We have a range of interest rates available at different prices. The lower the interest rate, the greater the cost.

In addition, you may have heard that interest rates change every day. It's not actually the interest rates that change; it's the cost to get a particular interest rate that changes. Today, I might be able to get an interest rate of 3.5% at a cost of 1% (of your loan amount). Tomorrow, 3.5% might cost 0.75%. Or it might cost 1.25%.

The cost to obtain an interest rate is also referred to as "discount points." One point equals one percent of your loan amount.

The trick with points is you want to balance the cost with the savings on your monthly payment. If you were given the opportunity to pay $5,000 in points to save $100/month on your payment, you'd probably take it, right? That's a good deal. But if you had to pay $5,000 in points to save $2/month on your payment, you might think twice.

Here's a hypothetical example using a $320,000 loan amount.

So the question to ask in the example above: Does it make sense to pay an additional $3,600 (the difference between 3.25% and 3.625%) to save $66/month on the payment? That's a question only the consumer can answer based on how long they think they'll keep the loan, their tolerance for debt, and their ability to make the payments.

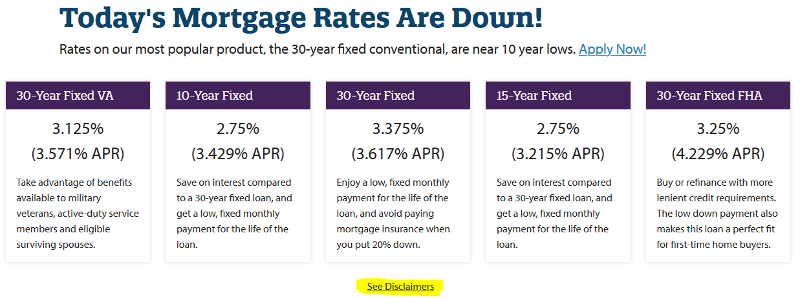

Keep in mind that many lenders (especially lenders that operate exclusively online) deliberately advertise uber low rates to lure you in, hoping you won't notice (or care about) the points associated with that rate. In the advertisement below, 2.75% sounds like a great deal for a 15-year fixed home loan, right?

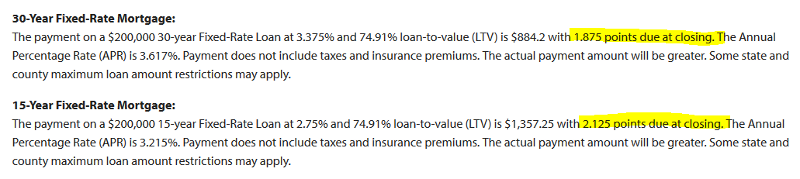

But when I dig a little deeper, I find that interest rate comes with 2.125% in points! In our $320,000 loan amount example above, that's $6,800 just for the interest rate!

You might make a different decision about paying points if you are purchasing a home versus refinancing. When you purchase a home, the closing costs (including any points) must be paid at closing. That's cash out of your pocket. But when you refinance, you can roll the closing costs into the new loan. You may be more willing (and able) to finance $4,000 than you are to come up with $4,000 out of your savings account.

If your loan amount is relatively low, you may also be more willing (and able) to pay points. Since points are a percentage of the loan amount, the lower the loan amount, the lower the cost. One point for a $400,000 loan is $4,000. But one point on a $100,000 loan is only $1,000.

Of course, the payoff isn't as great either. If you only owe $100,000, the difference between a 3% interest rate and a 3.5% interest rate is only $27/month. If you owe $400,000, the difference between 3.25% and 3.5% is $110/month.

You'll also notice that the highest interest rate in the chart above offers a lender credit instead of a cost. While you can pay extra to lower your interest rate, it also works the other way around. You can choose a higher interest rate in exchange for a lender credit toward closing costs.

Sometimes you'll hear lenders offering "no cost" refinances. That's how they do it. With very few exceptions, refinancing isn't free. The appraiser doesn't work for free. The escrow company doesn't close your loan for free. Instead, the lender offers you a higher interest rate, then uses the rebate pricing to pay your closing costs.

Just remember what your mom always told you: "If it sounds too good to be true, it probably is." While interest rates are at historic lows, few things in life are free!